Disclosure: This post may contain affiliate links. All credit cards mentioned are ones I personally hold or have held. This is not financial advice — it is my honest experience and perspective to help you think more critically about your own decisions.

There is no shortage of people telling you which travel credit card is the best in Canada.

Every bank has a recommendation. Every points blogger has a ranking. And somehow, every list seems to conclude that whatever card pays the highest affiliate commission is the one you should apply for.

I am going to do this differently.

This post is for Canadians who want their everyday spending to turn into actual travel, not just a points balance they never know how to use.

I spent years as an investment advisor at TD Canada Trust starting at 19, helping hundreds of clients make financial decisions, including credit products.

I have personally held every card I am recommending in this post. And I have worked with enough clients to know that the wrong card, even one with a massive welcome bonus, can cost you years of wasted earning potential.

One of my clients came to me after spending years (from university through her early thirties), earning CIBC Aventura points. She had never been able to use them for a single premium flight.

It wasn't that she did not accumulate enough, but because she had the wrong card for her goals from the beginning, and nobody told her.

That decade of spending cannot be recovered.

The cards I am recommending here are not universally the best cards in Canada. They are the ones I personally use, the ones I recommend most often to my clients, and the ones I can speak to honestly based on real experience.

I’ll tell you exactly who each card is for and who it is not for, whether you care most about premium flights, flexible points, lounge access, or avoiding cards that look better on paper than they are in real life.

Because the best travel credit card in Canada is the one that gets you where you want to go. Understanding

how travel rewards points work is very important when making your pick.

My Best Travel Credit Card Picks in Canada at a Glance

Accurate as of April 2026: Credit card offers, welcome bonuses, earn rates, annual fees, and perks can change often. Always confirm the current offer and terms directly with the card issuer before applying.

Before we get into the strategy, here are my honest picks based on who each card is best for.

Best Beginner Travel Credit Card in Canada

TD First Class Travel Visa Infinite

Best for Canadians who want an easy, low-friction way to understand how travel rewards work without learning award charts, transfer partners, or complicated redemption strategies.

Best Travel Credit Card for Food and Dining Spend

American Express Cobalt

Best for Canadians who spend heavily on groceries, restaurants, coffee shops, food delivery, and subscriptions, and want to build flexible points for future travel.

Best Travel Credit Card for Aeroplan and Air Canada

TD Aeroplan Visa Infinite

Best for Canadians who fly Air Canada or Star Alliance partners and want to build toward international redemptions, including premium cabin flights.

Best Premium Travel Credit Card for High Travel Spend

American Express Gold Rewards Card

Best for travelers with significant travel spending who want to earn transferable points on flights, hotels, car rentals, cruises, gas, groceries, and drugstores.

Best Business Travel Credit Card in Canada

RBC Avion Visa Infinite Business

Best for business owners who want to turn business expenses into premium travel, especially on airlines outside the Aeroplan and Star Alliance ecosystem.

The important thing is not just which card is “best.” The important thing is whether the card earns the type of points that can actually get you the trip you want.

The biggest mistake beginners make is asking, “Which card is best?” before asking, “Which points do I actually need?”

Before You Pick a Card, Know What You Are Picking It For

Most people approach travel credit cards the same way they approach choosing a restaurant on a Friday night.

They Google the best options, pick the one that looks good, and commit without really thinking about whether it fits what they actually wanted.

That works fine for dinner.

It can cost you years when you do it with a credit card.

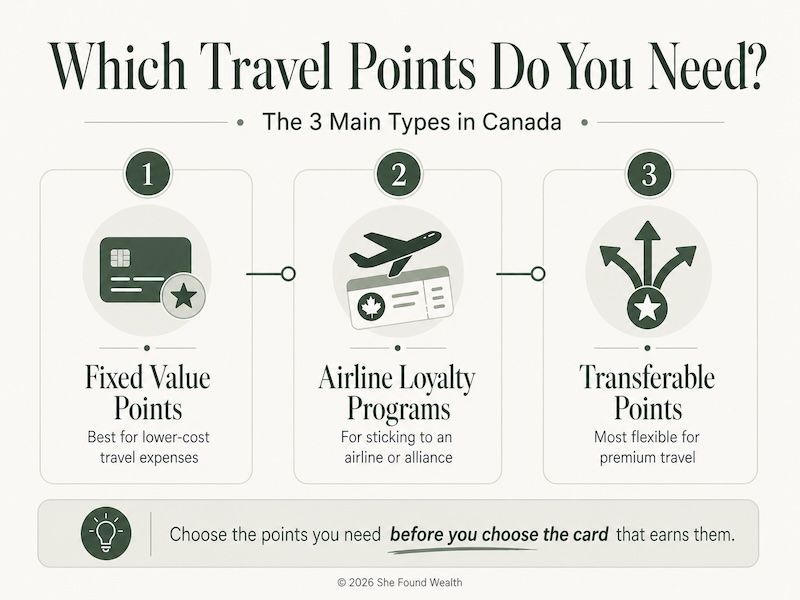

There are three main types of travel points in Canada that actually matter when you are choosing a card for travel rewards:

fixed value points, airline loyalty programs, and transferable points.

Cash back exists, and it can be useful for simple savings, but it is not usually the system that gets you into premium cabins.

For this post, I am focusing on the points systems that matter most if your goal is turning everyday spending into better travel.

I cover this in depth in my travel rewards points guide

How Do Travel Rewards Points Work in Canada, but here is the short version as it applies to choosing a card.

There are three main types of travel points in Canada that matter most when you are choosing a travel credit card:

- Fixed value points

- Airline loyalty program points

- Transferable points

The card you choose determines which type of points you earn. And the type of points you earn determines what is actually possible when it is time to redeem.

That is why you should never start with the card.

You start with the trip.

Fixed Value Points

Fixed value points, like TD Rewards or Scene+, usually have a predictable redemption value.

For example, a program might value points at something like 100 points = $1, depending on the redemption method and program rules.

These points are best for offsetting lower-cost travel expenses like economy flights, hotels, rental cars, vacation expenses, and sometimes even meals abroad.

They are easy to use, but they usually do not unlock the highest-value redemptions because it takes a long time to earn enough for a premium cabin flight.

That does not make them bad.

It just means you need to know what they are good for.

Fixed value points helped me save thousands of dollars over the years. When I first started using points, I was definitely an economy flyer. I was not thinking about first class. I was thinking, “How do I make these points stretch as far as possible?”

And for that stage, fixed value points served me really well.

I used them for flights, hotels, car rentals, and even meals abroad.

So I do think they have a place in a smart travel rewards strategy.

But if your goal is business class to Europe or a premium cabin flight to Asia, fixed value points are usually not the most efficient tool.

I still like having access to fixed value points for certain travel costs, especially hotels, car rentals, or cheap short-haul economy flights.

But I would not build my entire premium travel strategy around them.

Airline Loyalty Programs

Airline loyalty program points, like Aeroplan, are earned through co-branded cards and redeemed through the airline’s loyalty program.

This is where outsized value starts to appear.

These points can unlock international flights, partner airline redemptions, and premium cabin seats that would cost thousands of dollars in cash.

The tradeoff is that you are usually working within a specific airline or airline alliance.

In plain English: airline loyalty programs are best when you are willing to stick to an airline or alliance because that is where the redemption value lives.

That can sound restrictive at first, but it is not always as limiting as beginners think.

For example, I have used Aeroplan points to fly partner airlines like United, Lufthansa, and Singapore Airlines.

Even though Aeroplan is Air Canada’s loyalty program, Air Canada is part of Star Alliance, which gives you access to a much larger airline network.

Air Canada boasts that the Star Alliance is the most comprehensive airline network.

That is why Aeroplan can be so strategic for Canadians.

You are not limited to only flying Air Canada. You are often using Air Canada’s loyalty program to access partner airlines, different routes, and different cabin products.

You should also know that Aeroplan is free to join. You do not need an Aeroplan credit card to have an Aeroplan account, and you can earn Aeroplan points in other ways through everyday spending partners.

But if Aeroplan is part of your premium travel strategy, the right credit card can help you earn those points much faster.

Transferable Points

Transferable points, like American Express Membership Rewards and RBC Avion, are the most flexible.

You earn them through a credit card and can move them to multiple airline or hotel programs depending on where you want to go.

In plain English: transferable points give you more doors to walk through.

If one airline program does not have the flight you want, another one might.

This matters because some routes are competitive. Flights to places like Japan, Italy, or other popular long-haul destinations can be hard to find at the exact dates and cabin class you want.

The more options you have, the better.

That is why transferable points are so powerful. With American Express Membership Rewards, for example, you can transfer points to different airline partners, including programs connected to multiple airline alliances.

This gives you more flexibility than being locked into one redemption path.

I have personally used transferable points to top up another program when I did not have enough points for the flight I wanted. For example, when I needed more Aeroplan points to fly to Germany in business class, I transferred some of my Amex points to Aeroplan.

A lot of people do not even realize this is possible.

And it is one of the most slept-on strategies in Canadian travel rewards.

The key is that you usually get better value by transferring points to the right travel partner instead of redeeming them through a basic points portal.

Not always.

But often enough that it is one of the first strategies I want beginners to understand.

Before you choose a card, figure out the trip you are actually building toward.

The First Class Calculator helps you estimate how many points you need before you commit to a card strategy.

The Annual Fee Myth

Before we get into the individual cards, I need to address something I hear constantly:

“I only want a card with no annual fee.”

I understand the instinct.

Why pay for something when you can get it for free?

But here is the reality:

not one no annual fee travel card in Canada will get you a premium cabin flight in a reasonable timeframe. Not one.

Unless you are spending an unusually high amount every year, the earn rates on no annual fee cards simply do not accumulate points fast enough to make premium travel achievable.

I had a friend who told me she did not want to switch her card because she got free groceries from her current no annual fee card.

I understood the appeal.

Free groceries are tangible and immediate.

But she travels regularly and has always wanted to fly in premium cabins.

So I asked her to think about it differently.

When you learn how to use travel rewards strategically, you are paying pennies on the dollar for travel.

We are talking about nearly free travel. People are paying less in taxes and fees for premium cabin flights than they would pay in cash for an economy ticket.

You are not just saving on the ticket price.

You are getting a completely different and far more luxurious experience for less than the cost of what most people consider the budget option.

The opportunity cost of staying in a no annual fee program when premium travel is your goal is not just financial.

It is experiential.

Every year you spend earning slowly toward nothing meaningful is a year you are not arriving rested, comfortable, and ready for the trip you worked hard to take.

Groceries are useful. But if your real goal is premium travel, your card needs to be earning toward that goal.

The cards I hold have annual fees ranging from around $120 to $250. None of them feel expensive to me because every single one is paying for itself many times over through points earned, perks used, and travel covered.

The question is never just, “How much is the annual fee?”

The question is:

Is this card delivering more value than it costs me?

That is the only number that matters.

And depending on your banking setup, there may be ways to reduce or waive certain annual fees. Some premium bank accounts include annual fee rebates for eligible credit cards, so this is worth checking if you already bank with the issuer.

That does not mean you should open a bank account only for a fee waiver without doing the math.

It means the annual fee is one piece of the larger system.

I used to think differently about this.

When I worked at the bank, I had access to cards without paying the annual fees, so I became very resistant to paying for a different card elsewhere. I thought, “Why would I pay for a card when I can get one for free?”

But that mindset kept me stuck in programs that were not helping me get outsized travel value.

Now I look at it differently.

If a card costs $150 but helps me unlock $1,000 or more in travel value, that fee is not the problem. The problem would be refusing to pay the fee and staying in a program that does not get me where I actually want to go.

That does not mean every annual fee is worth it.

It means you need to look at the numbers.

If the card gives you more value than it costs, it is doing its job.

If it does not, it is not the right card for you.

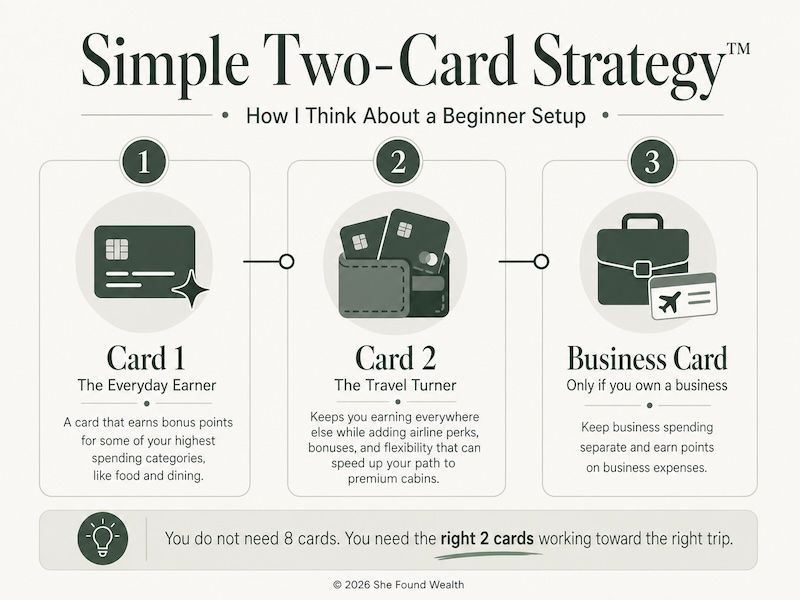

The Two-Card Strategy

The points and miles world has a tendency to make everything more complicated than it needs to be.

You will find people online juggling eight cards, tracking rotating bonus categories, and optimizing every single transaction down to the cent.

That is a hobby in itself. There is nothing wrong with it if that level of detail excites you.

But most people do not need it.

And honestly, most people will not stick with a system that requires that much maintenance.

I go through phases where I track everything closely. I am not going to pretend I never optimize or chase points.

But even as someone who is immersed in this world, there are seasons where I want a laid-back strategy too.

Recently, I have been focusing on my two-card strategy and not overcomplicating it. That gives me a simple system I can fall back on while still earning meaningful points toward the trips I actually want.

And it works.

I travel multiple times a year, more than the average person, and I still use points for long-haul flights that would cost thousands of dollars in cash.

I have even booked Qatar Airways from Montreal to Bangkok in business and first class using points — a trip that would have cost around $20,000 in cash. That particular trip had to be canceled because of the geopolitical climate, but the point still stands: the strategy made that redemption possible, and my out-of-pocket cost was under $1,000 round trip.

That is what most beginners need to understand.

You do not need to do everything.

You need a system that works.

When you try to do too much too quickly, it becomes easy to make mistakes. I have seen people get excited, open too many cards, forget about annual fees, miss deadlines, or get declined because they moved too fast without a plan.

That is not the goal.

The goal is to build a system you can actually maintain.

My philosophy is simple: two personal cards that work together toward your travel goals, and a business card if you own a business.

That is it.

Why Two Cards Works

No single card is the best card for every situation.

Practically speaking, not everywhere accepts every card. If your main earner card is an Amex, your second card might be a Visa or Mastercard backup.

It might also be a card that adds perks like free checked bags, airline bonuses, or access to points your everyday card does not earn.

There is also the practical reality that if there is ever an issue with one card, you are not stuck earning nothing while you sort it out.

I have had moments where I went to use a card and, lo and behold, it did not work. In those moments, having a second card is not just strategic. It is practical.

Could you use debit instead?

Sure.

But I personally hate using debit for a big purchase because it means I am earning nothing back. If I am already spending the money, I want that purchase moving me closer to a trip.

But the real reason for two cards is strategic.

The two cards need to work together to earn you the points you actually need for the flights you actually want.

Your two cards do not need to earn into the same points ecosystem either.

Depending on where you want to fly and which cabins you want to access, you may intentionally build toward two different programs because certain airlines and cabin products are only available through specific transfer partners.

What matters is that every card in your portfolio is earning toward a flight you actually want to take.

How Business Cards Fit In

On the business side, your card strategy is entirely separate.

Business expenses run through a business card, full stop.

Mixing personal and business spending muddies your financial picture and leaves points on the table.

If you own a business, your business card strategy runs parallel to your personal strategy, not on top of it.

Depending on your business structure, spending patterns, and travel goals, it may involve one card or more than one.

And just like with personal cards, your business card should match your actual travel goals.

The RBC Avion Business earns transferable points, which can be incredibly powerful. But if your goal is specifically to fly Air Canada or Star Alliance partners as often as possible, RBC Avion may not be the most efficient business card for your strategy.

That is why I always come back to the same point:

the card follows the goal.

Some people are loyal to a specific airline or cabin product. I have had clients who only want to fly one airline and are not interested in alternatives. There are British Airways loyalists, Delta loyalists, and people who simply prefer the cabin experience they already know.

That is not wrong.

But it does mean the card strategy needs to match that preference.

If you are loyal to a specific airline, you do not want to spend years earning points in a program that does not help you book the flights you actually want.

The RBC Avion Business is the card I recommend most often as the anchor of a business card strategy for premium travel, but it is a starting point, not necessarily the whole picture.

There is one exception to separating your business from personal expenses that I use personally, but it is an advanced strategy that requires having your financial and accounting systems completely dialed in and a close working relationship with your accountant.

It is not something I recommend until you are firmly at that stage.

My Honest Picks for the Best Travel Credit Cards in Canada

Every card I am recommending below is one I personally hold or have held.

I am going to tell you what I use it for, who it makes sense for, and just as importantly, who it does not make sense for.

Because a card that is wrong for your situation is not a good card, no matter how many points it promises.

If You Are a Beginner or Want to Prove Travel Rewards Actually Work

TD First Class Travel Visa Infinite

This is where I started.

My very first credit card was a TD Rewards card, and when I became eligible, I moved up to the TD First Class Travel Visa Infinite.

It was a natural progression and it served me well for years.

This is a fixed-value TD Rewards card, which means the points have a set value rather than being redeemed through an airline award chart.

That sounds like a limitation, and in some ways it is.

But for a beginner, it is actually an advantage.

You do not need to learn how to navigate award availability, transfer partners, or redemption sweet spots. You charge a travel purchase to the card, you redeem your points against it, and the cost comes off.

Simple. Immediate. Satisfying.

In 2023, I used this card to book six flights for zero dollars.

One of the things that makes this card particularly useful is that it does not charge taxes and fees on redemptions the way some other programs do, which means your points genuinely cover the full cost.

For those six flights, I was not limited to one airline alliance. I could book across different airlines, and my points still covered the flights.

That is where fixed-value points can be incredibly beginner-friendly.

They may not unlock the same outsized premium cabin value as airline loyalty programs or transferable points, but they are simple, flexible, and easy to use.

At the time of writing, the welcome bonus is 145,000 TD Rewards points after spending $7,500 within the first six months.

At a redemption rate of 200 points per dollar, that is approximately $725 in travel value from the welcome bonus alone.

This offer is listed as ending September 4, 2026. The card also currently includes perks like a

$100 hotel credit on eligible bookings through Expedia for TD and a birthday bonus.

When I held this card, it also came with limited-time promotions that added extra value for me, including a free Uber Eats benefit for a period of time.

Those kinds of promotions change, so I would never choose a card based only on a temporary perk. But they can make a good card even more valuable when the timing lines up.

Always check the current offer before applying, as these details shift periodically.

Who This Card Is For

This card is best for beginners who want a low-friction way to see travel rewards work.

It is also a good fit for people who want to offset economy flights, hotel stays, and car rentals without learning a complex system.

The TD Rewards card can also make sense for students or people who are not yet eligible for premium cards and want to start building their travel rewards foundation.

Who This Card Is Not For

This is not the card I would choose for someone chasing international business class or first class.

It is not the card that gets you into premium cabins efficiently.

It is the card that proves the system works and gets you comfortable with using points for travel.

If You Spend a Lot on Food, Dining, and Subscriptions

American Express Cobalt

In Canada, the Amex Cobalt is what I call an

earn card.

This is not a card you get because the welcome bonus is the entire strategy.

It is a card you get because over time, if your spending patterns align with it, it can accumulate American Express Membership Rewards points faster than almost anything else available to Canadians.

The earn rates are 5x points on eligible food and dining, including restaurants, quick service restaurants, coffee shops, stand-alone grocery stores in Canada, and food and grocery delivery services.

That 5x rate applies up to a combined maximum of $2,500 in net purchases per month across those categories. Once you hit that $2,500 monthly threshold, additional spending in those categories earns at the base rate.

The card also earns 3x on eligible streaming subscriptions and 2x on gas, transit, and rideshare.

For a lot of Canadians, food is one of their biggest monthly expenses.

If that is true for you, this card works exceptionally hard on your behalf without you having to think about it.

American Express Membership Rewards points are a transferable currency, which means they are not locked into one program.

You can transfer them to Aeroplan, Air France KLM Flying Blue, British Airways Executive Club, and several other partners depending on where you want to go.

I have personally transferred Amex points to Aeroplan and British Airways, and that flexibility is exactly why I value the program so much.

In plain English: this card helps turn everyday spending into points that can eventually become premium flights.

That is why it is one of the first cards I look at when someone tells me they spend a lot on groceries, restaurants, takeout, or coffee.

What About Amex Acceptance in Canada?

I hear this concern less and less.

The reality is that many restaurants, grocery stores, and everyday retailers in Canada now accept Amex. It is not the barrier it once was.

And since this card works best in exactly the categories where Amex is commonly accepted, it is rarely an issue in practice for the way I use it.

That said, I still recommend pairing it with a Visa or Mastercard so you are covered when Amex is not accepted.

Who This Card Is For

This card is best for anyone with high food, dining, grocery, coffee, restaurant, or delivery spend.

It is also a strong fit for people building toward transferable points for international travel.

For many Canadians, this is the natural first card in a two-card Amex strategy.

Who This Card Is Not For

This card is not ideal for travelers who primarily do all-inclusive trips where they are not putting much food spend on the card.

It is also not the best fit if your spending does not align with the bonus categories.

And because it is an Amex, I would not rely on it as your only card. It works best as part of a two-card setup.

If You Want to Fly Air Canada and Star Alliance Partners

TD Aeroplan Visa Infinite

This is my core Aeroplan card and the one I pair with the Amex Cobalt as my two-card personal strategy.

Where the Cobalt earns aggressively on food and everyday spending, the TD Aeroplan Visa Infinite builds my Aeroplan balance through travel purchases and Air Canada flights specifically.

Aeroplan is the program that unlocks the outsized redemptions.

Business class to Europe. Star Alliance partners across dozens of international routes. Long-haul flights that would cost thousands of dollars in cash.

This is the card that sits at the foundation of a premium travel strategy for many Canadians who fly Air Canada or its partners.

One perk that gets overlooked is that simply holding this card can give you free checked baggage when flying Air Canada. You do not necessarily need to book the flight with the card to access the checked bag benefit, as long as the card is properly linked to your Aeroplan account and the terms are met.

That alone can make a meaningful difference if you fly Air Canada regularly.

Since I also have Aeroplan Elite Status, I personally get additional Air Canada benefits, including two checked bags, Zone 2 boarding, and occasional preferred seats with extra legroom when flying economy.

Those perks come from my status, not just the card, but they are part of why Aeroplan has become such a core program in my travel strategy.

The TD Aeroplan card can also be useful when Aeroplan runs promotions through the Aeroplan eStore, especially when there are bonuses for using an Aeroplan credit card on eligible purchases.

If you fly Air Canada even a handful of times a year, the checked bag benefit alone can cover a significant portion of the annual fee.

At $30 to $65 per checked bag per flight, it adds up faster than most people realize.

A Note on Welcome Bonuses

I will be transparent about the welcome bonus landscape here.

When I was building my points strategy earlier in my journey, I was able to maximize welcome bonuses by strategically cycling between cards within TD’s lineup and timing the 12-month Aeroplan eligibility window.

That approach worked well for me for years.

The terms have since changed, and Aeroplan no longer allows you to earn a welcome bonus on a card you have previously held.

The landscape evolves and what worked then does not work now, which is exactly why staying current on program terms matters.

Who This Card Is For

This card is best for anyone whose primary travel is on Air Canada or Star Alliance partner airlines.

It is also a strong fit for people building toward Aeroplan redemptions for international premium travel.

And if you fly Air Canada regularly and want to stop paying for checked baggage, this card can quickly become worth it.

Who This Card Is Not For

This card is not ideal for travelers who primarily fly WestJet or airlines outside the Star Alliance network.

It is also not the best fit if your dream flights require programs Aeroplan cannot access, like Qatar Airways or certain other premium carriers.

If You Travel Heavily and Want to Maximize Every Dollar Spent on Travel

American Express Gold Rewards Card

The Amex Gold is the card I reach for when my travel spend is high and I want to make sure every dollar is earning meaningfully.

It earns 2x American Express Membership Rewards points on eligible travel purchases, including flights, hotels, car rentals, and cruises.

It also earns 2x on gas, groceries, and drugstore purchases.

Here is how it fits into my strategy.

The Amex Cobalt earns 5x on food and dining up to its $2,500 monthly threshold.

When I hit that threshold in a heavy spending month, I switch to the Amex Gold for the remainder of that category and still earn 2x rather than dropping to the Amex Cobalt base rate of 1x per dollar.

It is a natural complement rather than a duplicate.

Where the Gold really earns its place in my portfolio is on travel charges.

I travel a lot, and I do not always book flights with points, especially domestic and short-haul flights.

For a long time, I used the Gold as part of my broader travel strategy. My approach is to prioritize points for international premium cabin travel and use cash for other travel expenses when that makes more sense.

When I do pay cash for eligible travel expenses, I like charging them to the Amex Gold so I can still earn 2x points.

I have also used it for travel expenses while abroad, which helped me keep building my Amex Membership Rewards balance even when I was not redeeming points for that specific trip.

Over the course of a year of heavy travel, that can accumulate into a meaningful points balance.

Who This Card Is For

This card is best for frequent travelers with high travel spend who want to earn transferable points on those purchases.

It also makes sense for existing Amex Cobalt holders who want a complementary card for overflow spending in bonus categories.

If you are building a larger American Express Membership Rewards balance for flexible redemptions, this card can fit well.

Who This Card Is Not For

This card is not the best fit for light travelers who do not charge significant travel expenses to their card.

It also makes more sense as a complement than as a standalone card.

If you do not already have a clear Amex strategy in place, I would usually start with the Cobalt first.

If You Own a Business and Want to Fly Premium Cabins

RBC Avion Visa Infinite Business

This card changed my points game entirely.

The RBC Avion Business earns 1.25 Avion points for every dollar spent, up to $75,000 per year.

That can be significant if you have regular business operating costs.

At the time of writing, it has one of the strongest flat earn rates I have found on a Canadian business card.

When you are running a business and putting significant expenses through a card every month, that consistent 1.25x on everything adds up to a substantial points balance faster than most people expect.

Within one year of getting this card, I used the Avion points I had accumulated to

pay for an international flight.

Here is what makes this card strategically important beyond the earn rate.

RBC Avion points transfer to a set of partners that includes some programs Aeroplan cannot access.

Qatar Airways, widely considered one of the best airlines in the world for premium cabin travel, is bookable through British Airways Executive Club, which is an Avion transfer partner.

So are Cathay Pacific, Japan Airlines, and American Airlines AAdvantage.

If your aspirational travel involves carriers outside the Star Alliance network, Avion gives you a pathway that Aeroplan simply does not.

I am planning multiple trips to Asia, and having access to those carriers through Avion is a core part of how I am building toward those redemptions.

You cannot fly Qatar Airways with Aeroplan.

You can with a strategy that includes RBC Avion.

Who This Card Is For

This card is best for business owners who want to earn premium travel points on business expenses.

It is also a strong fit for anyone with aspirational flights on carriers outside the Star Alliance network, like Qatar Airways, Cathay Pacific, or Japan Airlines.

If you own a business and want a strong flat earn rate on a Canadian business card, this is one I would look at closely.

Who This Card Is Not For

This card is not for employees without business expenses.

It is also not necessary for someone whose travel goals are fully covered by Aeroplan and Star Alliance partners.

And if you are not yet ready to manage a separate business card strategy, I would focus on getting your personal card setup right first.

How to Know If Your Travel Credit Card Is Actually Worth It

This is the question most points content never asks, and it is the most important one.

Getting a card is step one.

Knowing whether it is actually delivering for you is what separates someone who dabbles in travel rewards from someone who consistently gets value from them year after year.

Add Up What the Card Has Actually Given You

Not what it could theoretically give you.

What it has actually given you.

Look at:

- Points earned

- Perks used

- Travel covered

- Statement credits applied

- Lounge visits taken

- Baggage fees saved

- Insurance benefits actually used

Every card in your portfolio should have a real number attached to it that represents the value you extracted from it in the past twelve months.

Compare the Value to the Cost

Then compare that number to what the card cost you.

That includes:

- Annual fee

- Any interest paid if you ever carried a balance

- Foreign transaction fees

- Any other costs tied to keeping or using the card

That is your total cost.

If the value you received is higher than the cost, the card is working.

If it is not, something needs to change: your card, your spending habits, or how you are redeeming.

Check Whether Your Points Are Moving Toward Your Actual Goals

This is where a lot of people get stuck without realizing it.

They are earning consistently, but the program they are earning in cannot deliver the flights they want.

Points sitting in a program that does not serve your goals are not working for you, no matter how many you have accumulated.

I have seen clients come to me with hundreds of thousands of points they cannot use for a single flight they actually want to take.

That is why the card always follows the strategy.

Not the other way around.

Do Not Ignore the Perks

The cards in this post all carry perks that contribute to their value in ways that are easy to overlook.

Free checked baggage on Air Canada. Travel credits. Purchase protection. Emergency travel insurance.

I have personally received value from perks like free checked bags, lounge access, temporary memberships like Uber One, and discounts or credits at stores where I already planned to shop.

These perks are not the whole reason to choose a card, but they have real dollar values and should count toward your return on investment calculation.

I have a

calculator I use with my clients and students that walks through exactly this exercise, showing you whether a card is delivering based on your specific spending and travel patterns.

It takes the guesswork out and gives you a clear answer on whether to keep a card, upgrade, or move on.

The goal is not to have the most cards.

It is to have the right cards and know with confidence that each one is earning its place in your portfolio.

Common Questions About Travel Credit Cards in Canada

What Is the Best Travel Credit Card in Canada for Beginners?

The TD First Class Travel Visa Infinite is where I point most beginners.

It is straightforward, the points have a fixed value, and there is no complex redemption strategy to learn.

It is the card that proves the system works without requiring you to become a points expert overnight.

Once you are comfortable with how travel rewards function in practice, you can layer in more strategic cards from there.

What Is the Best Credit Card for Travel Points in Canada?

The best credit card for travel points in Canada depends on the kind of points you need.

If you want simple travel credits, a fixed-value card like the TD First Class Travel Visa Infinite can work well.

If you want premium cabin flights, transferable points and airline loyalty points usually matter more.

That is why I like cards like the Amex Cobalt, TD Aeroplan Visa Infinite, Amex Gold, and RBC Avion Business. Each one earns points that can support a specific travel strategy.

Is the Annual Fee Worth It on Travel Credit Cards?

For premium travel, yes, if the card is being used correctly.

Every card in this post charges an annual fee, and every one of them delivers more value than it costs when used for its intended purpose.

The calculation is simple: add up the points earned, perks used, and travel covered over the past year.

If that number exceeds the annual fee, the card is worth it.

If it does not, either you are not using the card correctly for your spending patterns, or it is the wrong card for your situation.

Can I Hold More Than One Travel Credit Card?

Yes, and for most people building toward premium travel, you should.

The two-card strategy I outlined in this post exists precisely because no single card optimizes every spending category or every travel goal.

Your two cards do not need to earn into the same points ecosystem either.

Depending on where you want to fly and which cabins you want to access, you may intentionally build toward two different programs because certain airlines and cabin products are only available through specific transfer partners.

The key is that every card in your portfolio is earning toward a flight you actually want to take.

If it is not doing that, it does not belong in your wallet.

How Do I Know Which Card Is Right for Me?

Start with your travel goals, not the card.

Where do you want to go?

How do you want to fly?

Which airlines operate those routes?

Once you know the destination and the experience you are building toward, you can identify which loyalty program gives you access to it, and then find the card that feeds that program most efficiently.

The card always follows the strategy.

Why Have I Earned Travel Points but Still Cannot Book Premium Flights?

Usually, it is because you are earning the wrong type of points for your goal, earning too slowly, or collecting points in a program that does not access the flights you want.

This is exactly what happened with the client I mentioned earlier who spent years earning Aventura points but could not use them for the premium flights she wanted.

The issue was not that she failed to earn points.

The issue was that her points were not connected to the travel goal she actually had.

That is why I recommend reverse-engineering your points strategy from the trip you want to take, not from the card a bank happens to be promoting.

What Is a Welcome Bonus and How Does It Work?

A welcome bonus is a lump sum of points offered by a credit card issuer to new cardholders who meet a minimum spend requirement within a specified timeframe.

Welcome bonuses are one of the fastest ways to accumulate a meaningful points balance quickly.

For many people, they cover the bulk of what is needed for a first redemption.

One thing worth knowing: welcome bonus chasing is a real strategy, but it is an advanced one.

It requires a thorough understanding of program terms, credit implications, and timing.

For most people who are not traveling at a very high frequency, it is not necessary and can get complicated fast.

Focus on building a solid card portfolio first.

The welcome bonus is a great head start, not the whole strategy.

Do Travel Credit Cards Affect Your Credit Score?

Applying for a new credit card results in a hard inquiry on your credit report, which can temporarily lower your score by a small amount.

Holding a card responsibly, meaning paying your balance in full every month and keeping your utilization low, generally has a positive effect on your credit score over time.

Travel rewards cards are designed for people who pay their balance in full.

That is the only context in which they make financial sense.

The Right Card Is the One That Gets You There

There is no universally best travel credit card in Canada.

Anyone who tells you otherwise is either selling something or has not thought carefully enough about what you are actually trying to accomplish.

The cards in this post are my keeper cards.

The ones I hold, use, and recommend because they have delivered real value in my own travel and for my clients.

But what makes them work is not the cards themselves.

It is having a strategy that connects your spending to your goals and your goals to the right program.

If you are a beginner, start with something that proves the system works and gets you your first win.

If food and dining is your biggest expense, earn 5x on every dollar of it.

If Air Canada is how you fly, build your Aeroplan balance intentionally.

If you own a business, put your business expenses to work in a program that can get you the cabins you want.

And if you have been earning points for years in a program that cannot deliver the flights you actually want, it is not too late to change course.

The thing that makes me most passionate about this is not the points.

It is what the points make possible.

Arriving in a flat bed seat on a twelve-hour flight and stepping off the plane feeling rested and ready.

Experiencing a cabin product you saved up for years and paid almost nothing for in cash.

Traveling more, traveling better, and keeping the money you save working for you in other ways.

That is what this is actually about.

Before you apply for a card, figure out how many points you actually need for the trip you want to take.

The

First Class Calculator helps you reverse-engineer your points goal so you are not guessing, collecting the wrong points, or wasting years on a card that cannot get you where you want to go.

And if you are still building your foundation on how travel rewards work before diving into specific cards,

learn how travel rewards points work in Canada!